The attacks on Iran by US and Israeli forces and the responses from Teheran have had an immediate and profound impact on airfreight flows. Iran’s attacks on Gulf hubs forced the closure of airports and grounded the fleets of airlines based in the region, which stranded almost half of the capacity with origin Middle East & South Asia last weekend, and about 15% of global air cargo capacity. The situation is fluid. Afflicted airports resumed operations by mid-week this week and the fleets of Gulf-based carriers ramped up their flights again. Forwarders have resorted to charters out of Asia Pacific amid warnings that backlogs of airfreight to Europe and the US could become an issue by the weekend.

As the attacks on Iran began on Saturday 28 February, data compiled by WorldACD for the week ending Sunday 1 March capture only the immediate impact of the first two days of the conflict. Our publication next week will give a clearer picture how the hostilities affect air cargo traffic, capacity deployment and rate development. What is clear is that air cargo flows suffered immediate disruption. The significance of the Middle East & South Asia region for the worldwide air cargo flows is well illustrated in our LinkedIn post earlier this week, showing that 21% of global air cargo traffic is directly impacted.

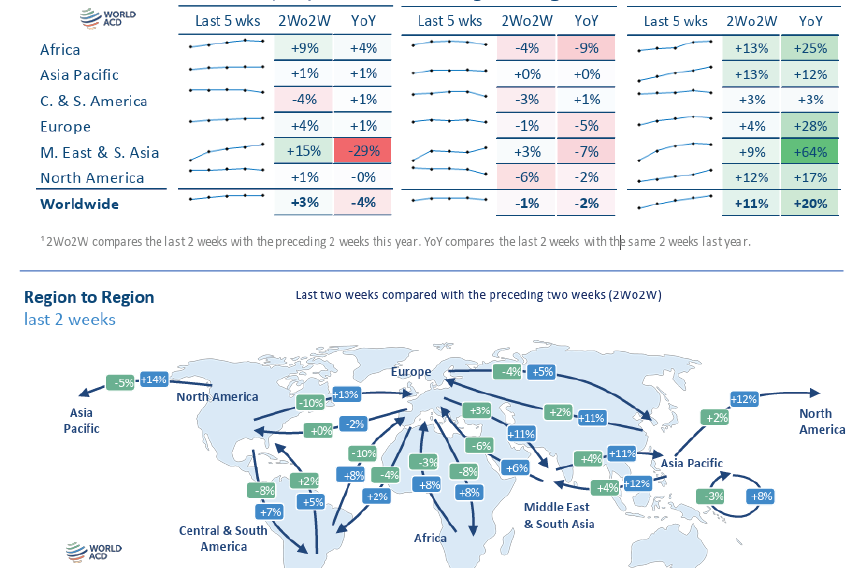

The latest weekly figures and analysis from WorldACD Market Data show pronounced slumps in traffic in immediate response to the outbreak of hostilities, with the Middle East & South Asia (MESA) showing the severest impact. Compared to the same day of the week of the preceding week (week 8), overall airfreight exports from the region fell -27% on Saturday 28 February, accelerating to -56% the following day for a combined drop of -40%. The Levant and Gulf area registered a week-on-week (WoW) slump of over -70% on Sunday 1 March.

Out of South Asia chargeable weight to Europe and the US fell -57% and -33% respectively for an overall decline of almost -50% on Sunday 1 March, compared to the previous Sunday (22 February). Traffic out of China and Northeast Asia to Europe turned south again (-4%) last weekend, after continuous improvement over the first five days of the week, while an -8% decline to Europe on the weekend slowed growth out of Southeast Asia.

Week 9 (23 February to 1 March) is a tale of two worlds, with five days of business as usual followed by two days impacted by the war in the Middle East, making interpretation of the weekly more challenging. While the Lunar New Year period officially came to an end on Tuesday 3 March, activity started already ramping up last week, with a +13% WoW jump in tonnages outbound Asia Pacific, leading to a global positive WoW growth figure of +2%.

Strong demand for servers and semiconductors fueled WoW volume surges of +66% and +54% from Taiwan and South Korea to the US, whereas tonnage from China and Japan fell by -5% and -9%, respectively. Pricing from Asia Pacific to the US rose +3% WoW, as double-digit increases out of Japan, South Korea and Malaysia were countered by lower rates out of China and Hong Kong. Year on year (YoY) pricing from Asia Pacific to the US was down -5% on double-digit drops out of Japan, South Korea, Hong Kong and Indonesia. To Europe spot rates from Asia Pacific slipped -3% due to decreasing rates out of China (-2%), Hong Kong and Japan (-3% each).

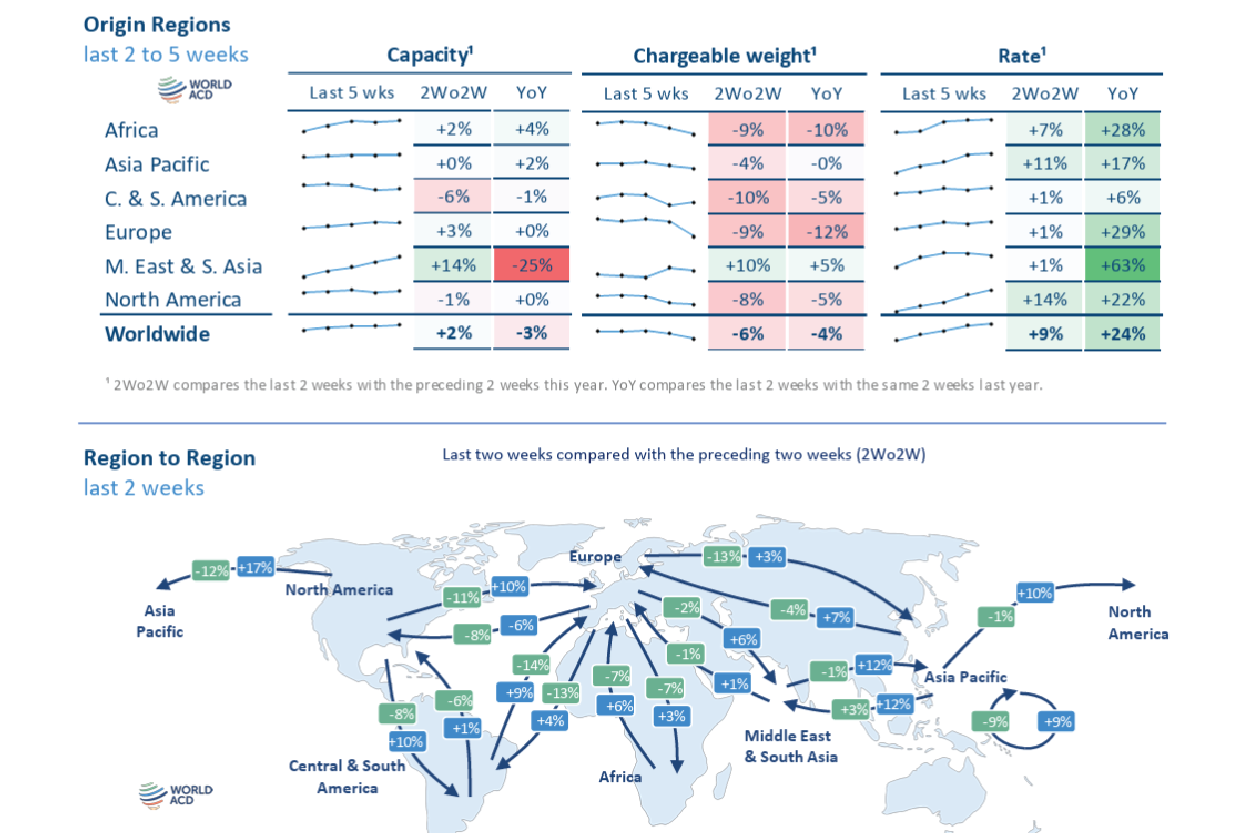

With the exception of MESA (+2%) and North America (unchanged), overall pricing retreated in all regions, led by a -8% drop in Asia Pacific. Global pricing decreased -3% WoW and -1% YoY. This points to a softening demand, as capacity has diminished. After a -7% drop in week 8, it shrank another -2% the following week. Compared to the same period a year ago, capacity in the past two weeks was flat, with gains in Africa (+15%), CSA (+8%) and Europe (+3%) cancelled out by drops in Asia Pacific (-4%) and MESA (-2%).

Following +8% growth in January, YoY, the industry clocked up a collective increase of +7% in chargeable weight for February. Except for Europe (down -3%) tonnage increased in all regions, with Asia Pacific volume rising +14% and traffic out of MESA up +12%. The picture is more uneven in terms of pricing. Rates out of Europe climbed +9%, while pricing from Asia Pacific and Africa rose +6% and +7% respectively. On the other hand, rates from MESA fell -8%, North American pricing was down -3% and rates from CSA diminished by -2%.

The hostilities in the Middle East have multiplied the uncertainty looming over global trade, from the prospect of prolonged warfare causing an economic downturn to severe restrictions of flight corridors linking Asia and Europe and galloping oil prices fueling inflation and airline surcharges. As we have seen this week, the air cargo industry will step up to the plate and once more show its resilience to keep global trade moving.

Source: WorldACD

Global air cargo rates have continued to rise despite a further drop in worldwide tonnages, linked to Easter holidays and additional bellyhold capacity returning to Gulf markets.

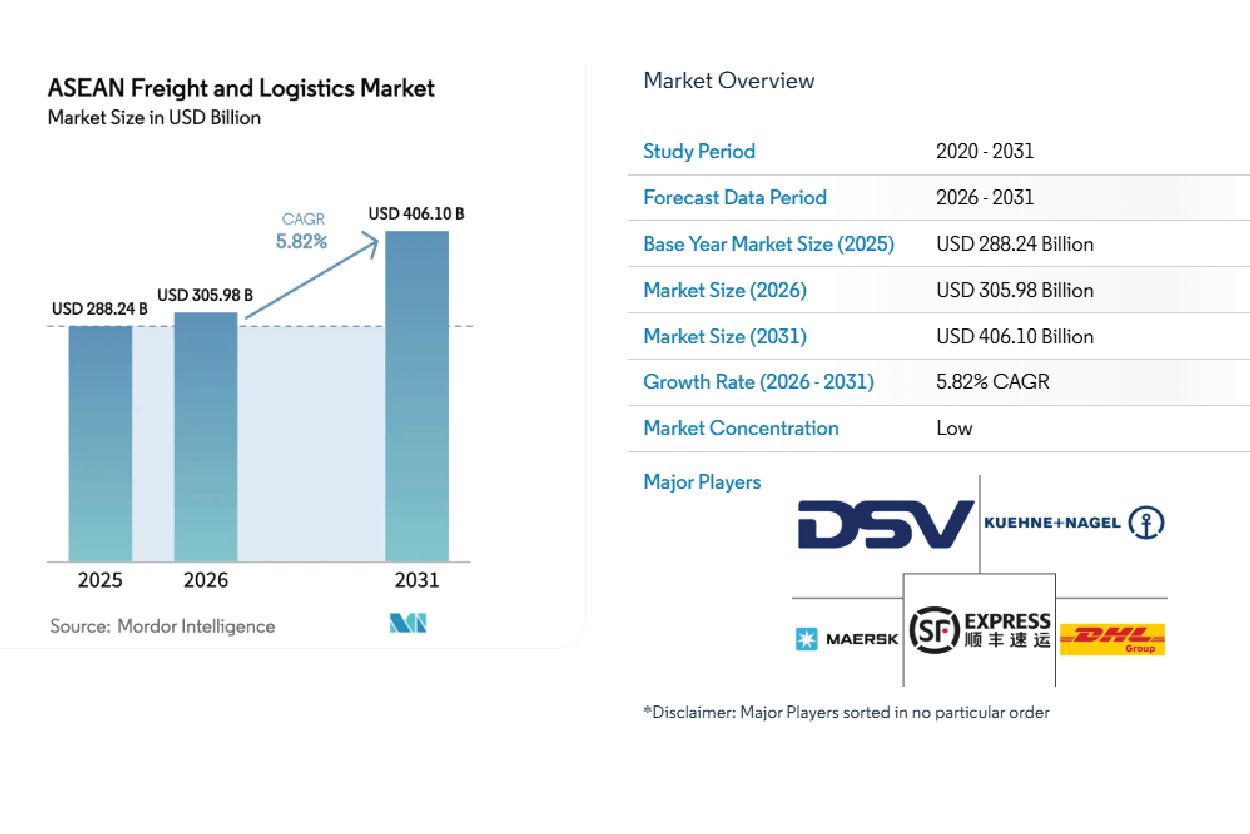

The ASEAN freight and logistics market size is projected to reach USD 406.10 billion by 2031, growing at a CAGR of 5.82% from 2026 to 2031.

Global air cargo networks adapt to Middle East airspace closures, rerouting through alternative hubs and longer paths, impacting cost, time, and trade.

The report concludes that competitive advantage will depend on how effectively organisations integrate AI, automation and analytics into end-to-end operations, rather than...

The infrastructure supporting air freight handling at airports has long been neglected. There are answers but funding is an issue.

Rising oil prices affecting air freight and blocks to shipping routes are forcing Asian logistics firms to rethink plans and absorb losses

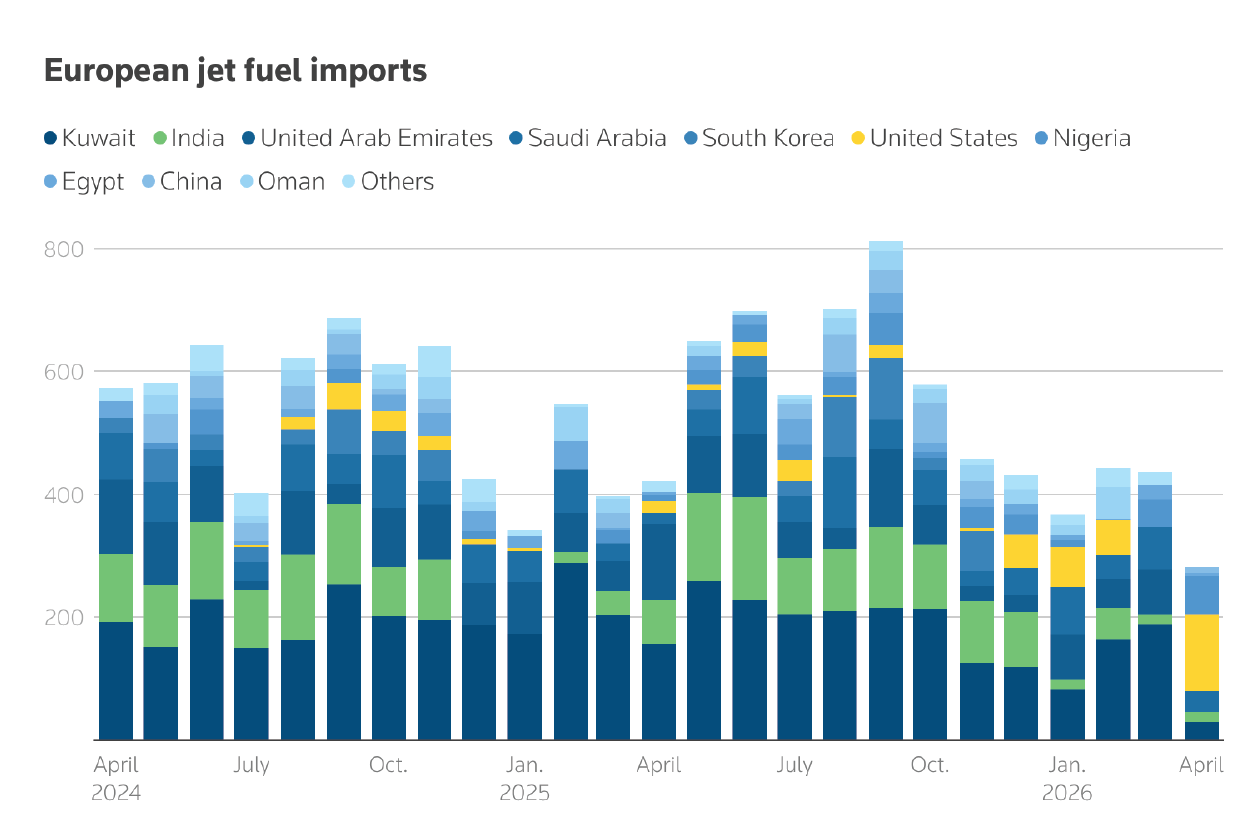

Flights in Europe could start to be cancelled from the end of May due to a lack of jet fuel

belly cargo decreased by 8%, mainly due to cancelled passenger flights to the Middle East.

The jet fuel crisis is no longer a short-term disruption. Even if geopolitical conditions stabilise, the structural impacts on fuel supply chains, refining capacity and global...

Air cargo exports from APAC declined -3% WoW to Europe and -1% to USA.