Global air cargo rates have continued to rise despite a further drop in worldwide tonnages, linked to Easter holidays and additional bellyhold capacity returning to Gulf markets.

According to the latest weekly figures from WorldACD Market Data, average worldwide spot rates rose by a further +3% in week 15 (6 to 12 April) to US$3.76 per kilo, taking them +37% higher than this time last year and more than +40% up compared with their level at the end of February, when the US and Israel launched military strikes on Iran.

The biggest week-on-week (WoW) increase among the main world regions came on spot rates from North America origins, which rose by +6%, WoW, to an average of $2.73 per kilo, +52% higher, year on year (YoY). Spot rates from Africa recorded a +4% further increase in week 15, to $2.95 per kilo, taking them +62% higher, YoY, while spot rates from Asia Pacific edged upwards by a further +2% to an average of $4.95 per kilo, up +24%, YoY.

From the Middle East & South Asia (MESA) region, average spot rates in week 15 actually edged back slightly (-1%) downwards, WoW, in week 15 to $4.81 per kilo, although that’s +66% higher compared with this time last year, with capacity to and from the region still highly disrupted despite the very considerable efforts and successes to reintroduce services and find alternative routings.

On the demand side, worldwide air cargo tonnages dropped by a further -6% in week 15, WoW, having fallen -3% the previous week, taking worldwide tonnages -8% below the equivalent week last year, based on the more than 500,000 weekly transactions covered by WorldACD’s data. The biggest WoW decline in chargeable weight was from Europe origins (-15%), linked to national holidays in many countries due to Easter, although there were also significant declines from Africa (-7%), Asia Pacific (-3%), MESA (-3%), and North America (-2%, WoW).

Worldwide air cargo capacity saw a further +1% WoW increase in week 15, led by an additional +7% recovery of capacity from MESA. Although global capacity has rebounded close to its levels this time last year, capacity from MESA origins remains down by around -20%, YoY. In weeks 14 and 15, combined, capacity from MESA was +14% higher than in the previous two weeks, although it remained -25% down, year on year. Despite that YoY capacity deficit, tonnages from MESA across those two weeks were slightly up (+5%), YoY – partly a reflection of the greater use of freighter capacity and high demand for capacity from the region, where ocean freight has also been facing serious capacity constraints, delays, and backlogs, but also partly helped by the impact of Eid-al-Fitr at the end of March last year.

Within the MESA region, air cargo capacity from South Asia has recovered to within -5% of pre-war levels, with new capacity direct to Europe largely replacing capacity previously linking South Asia with other airports within or via the MESA region. Tonnages from MESA to Europe in week 15 were actually up +3%, YoY, with volumes from India down slightly (-4%), while there was a big surge in traffic in week 15 from Bangladesh to Europe.

On the pricing side, average rates from MESA to Europe in week 15 were up by +89%, year on year, to $4.53 per kilo, including a +77% YoY increase from India, a +94% YoY rise from Bangladesh, and +71% YoY increase from Sri Lanka.

The two-week ceasefire agreement this month between Washington and Teheran raised hopes of a lasting settlement of the conflict, although the truce remains fragile and the outlook for peace is uncertain. Most observers have warned that inflation and elevated fuel costs are likely to persist for some time, even if the current ceasefire holds, and there are increasing concerns that jet fuel shortages and rising costs of jet fuel will lead to flight cancellations and further air cargo rate rises in the coming weeks unless there is a swift resolution to the current crisis.

Meanwhile, bellyhold capacity through the Middle East will take time to fully recover, and container lines do not expect a return to pre-conflict flows any time soon, meaning air cargo pricing is likely to remain elevated for some time.

Source: WorldACD

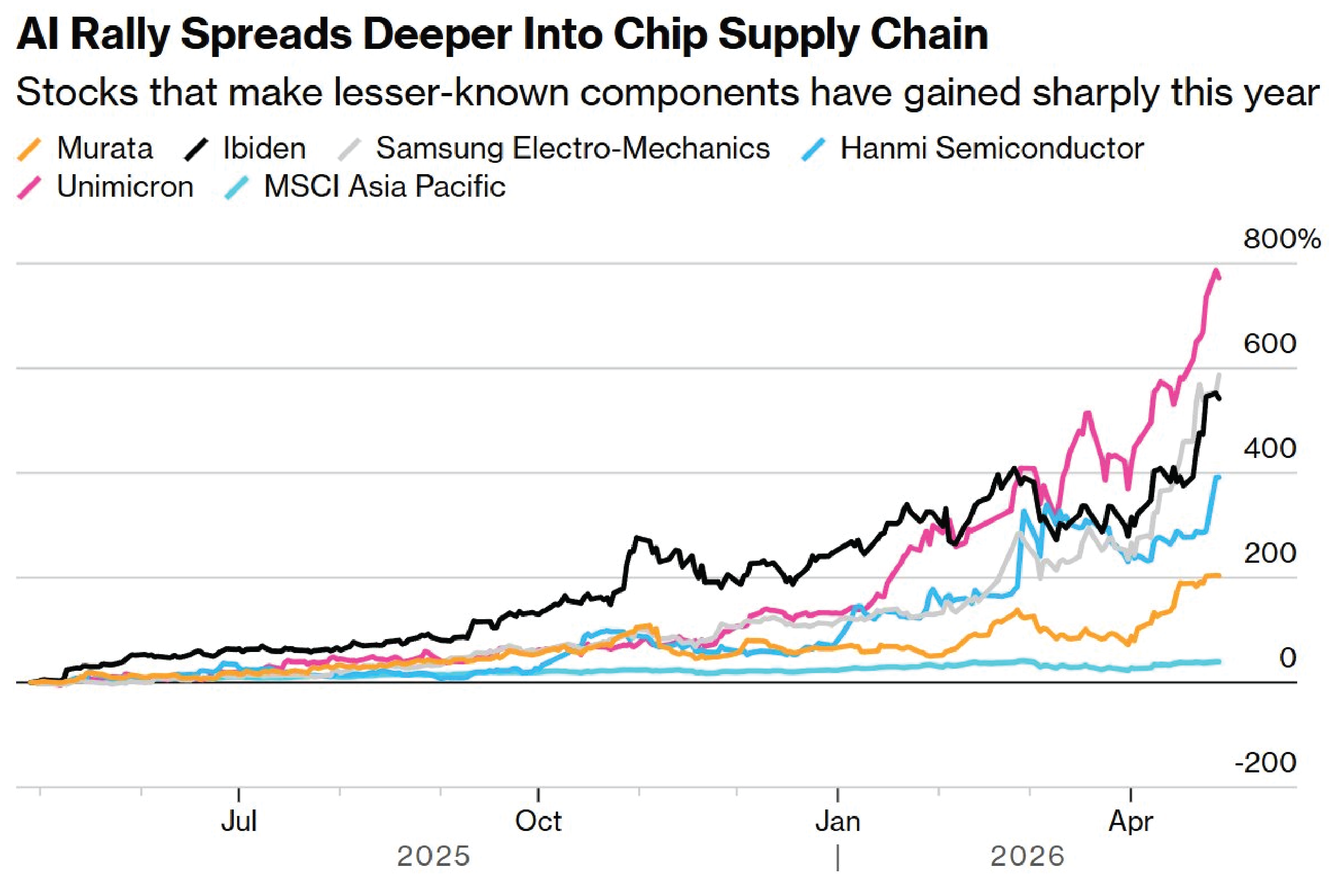

Apple’s chip supply chain still runs through Taiwan, but the AI boom is making that dependence harder to ignore.

ates from Europe to North America dropped 17% to $2.57 per kg, making it the only major corridor to see a decline. Even with demand growing 2% in April, the pressures facing...

DHL Express has launched an artificial intelligence-powered item identification feature for international shipping, introducing a system that uses computer vision to generate...

AI infrastructure demand is strengthening flows between technology manufacturing regions and major data centre markets.

United Cargo, Air Canada Cargo and Cathay Cargo are among the airlines implementing fees to buffer the impact of higher jet fuel costs.

Despite saying the levy was “unauthorized by law,” the U.S. Court of International Trade did not issue a universal stay, instead providing injunctive relief for three parties...

Airfreight capacity is continuing to come under pressure as a result of rising demand for AI and computer chip products and a reduction of bellyhold capacity

The artificial intelligence rally exploding across Asia is now spreading deeper into the supply chain.

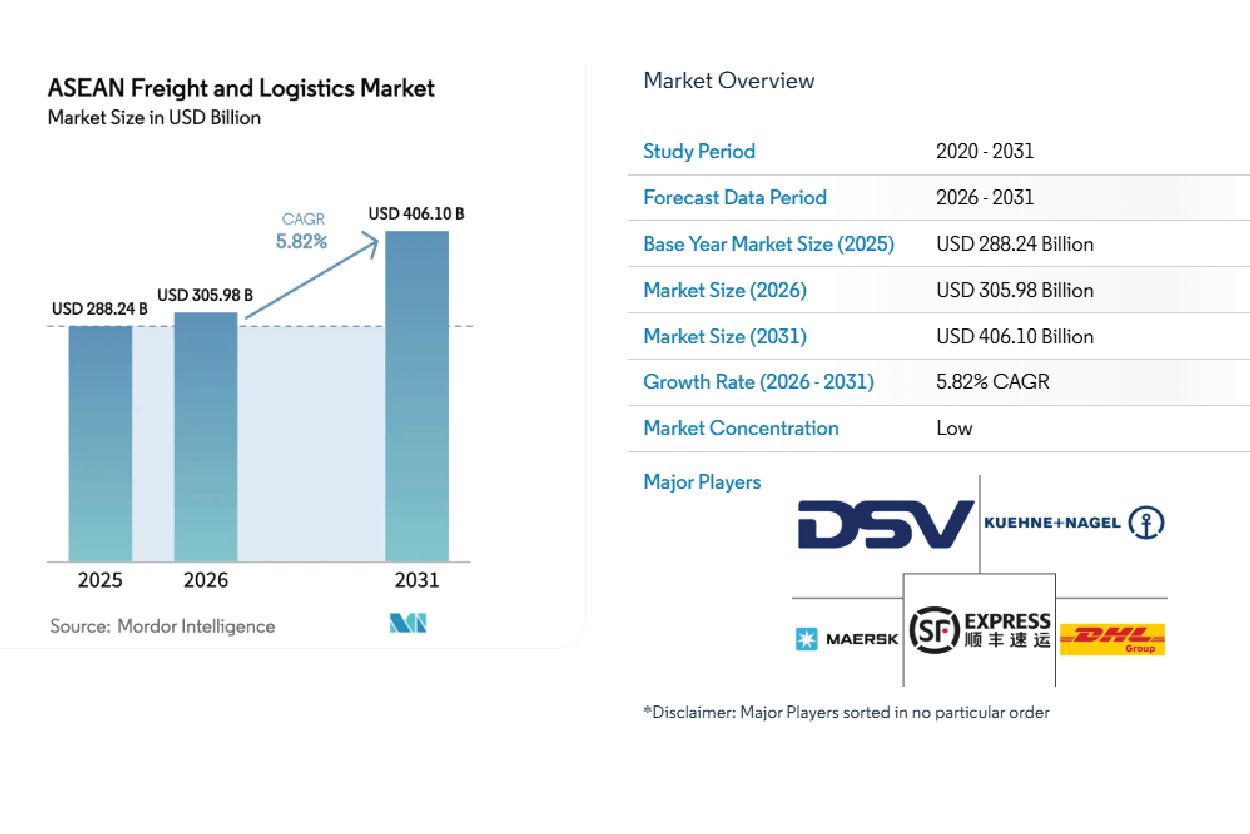

The ASEAN freight and logistics market size is projected to reach USD 406.10 billion by 2031, growing at a CAGR of 5.82% from 2026 to 2031.