Calendar-driven tightness and structural growth

Air freight in February often gets reduced to a single narrative: Demand out of Asia compresses ahead of Lunar New Year followed by a rapid decline. This year brings a notable distinction. While Asia is experiencing short-term, calendar‑related tightness, South Asia and South America continue to undergo steady, long-term structural changes. The difference isn’t just operational timing; it’s a fundamental distinction between volatility shaped by the calendar and growth shaped by long-term economic realignment.

Asia’s predictable compression window

Asia-Pacific’s familiar pattern has begun: a short, intense surge of demand in the first half of the month as factories close for Lunar New Year. Shippers compress what is normally four weeks of exports into roughly 12 days. Demand appears to be concentrated in the same time-sensitive sectors that have defined the region’s air market over the past several years: electronics, semiconductors, components for artificial intelligence, crypto-mining hardware, and solar technologies bound for the United States, alongside ecommerce and fast-moving consumer products moving toward Europe.

Capacity is expected to remain tight right up to the February 17 holiday window, then is usually self-correcting. Once factory production halts, outbound demand typically drops faster than airlines reduce schedules. By early March, Asia generally returns to a normalized balance of capacity and demand. This cycle is a predictable seasonal effect, not a structural one.

South America’s transition from export origin to bidirectional hub

Where Asia’s pattern is cyclical, South America’s appears to be undergoing lasting change. The region is shifting from a predominantly export-driven origin toward a bidirectional trade hub. Several forces appear to be moving in the same direction:

This month’s conditions reinforce that shift. Although there was a brief slowdown in volumes toward the end of last year, the region is still expected to grow over the long term. Perishable items such as flowers, fruit, and fish remain strong, forming a seasonal baseline that manufactured goods and cross-regional services are building upon. The introduction of new long-haul services, slated for full implementation early this year, suggests growing carrier confidence in sustained two-way trade opportunities rather than solely outbound demand.

Operational constraints—inland transport bottlenecks, customs delays, limited digitalization—still shape how evenly growth materializes. These challenges appear to be driven more by infrastructure frictions than underlying market weakness. Carrier capacity decisions suggest growing confidence in South America as a longer-term growth region, rather than a market driven primarily by seasonal demand.

Underlying demand in India and South Asia remains firm

South Asia presents a different structural pattern. India’s air freight demand for electronics, pharmaceuticals, and high-value goods appears to be transitioning from a premium or emergency option to an increasingly standard one. Supported by steady output in the technology and healthcare sectors and expanding long-haul connectivity across multiple major hubs, demand remains resilient even as other regions soften.

This structural consistency helps explain why congestion persists on certain lanes, despite easing global demand, as these commodities typically require air transport and offer limited flexibility to shift to alternative modes.

Europe’s softness reinforces the split

If Asia is tight for temporary reasons, Europe sits on the opposite end of the spectrum. Increased belly capacity on long-haul passenger flights and subdued manufacturing activity continue to limit Trans-Atlantic rate increases. This persistent softness underscores why Asia’s tightness shouldn’t be interpreted as a global trend. Instead, February’s market signals are a reminder that not all air freight operates under the same demand logic or planning horizon.

Different market cycles are emerging

Overall, February highlights the emergence of two distinct patterns in air freight economies:

These differing approaches affect how planning aligns across regions. In Asia, market conditions tend to favor short-term positioning and advance bookings, while South America and South Asia are increasingly shaped by longer-term trade development, influencing routing options, service availability, and capacity consistency.

Planning ahead

The key issue isn’t whether February causes tighter conditions in Asia—it always does. What’s important is whether shippers are updating their planning strategies to handle calendar‑related fluctuations in some areas and ongoing changes in others. Air freight trends aren’t consistent across the board, and February makes these differences especially noticeable.

India’s modal shift is reshaping air freight demand

India’s air freight sector appears to demonstrate an ongoing structural transformation that is shaping global capacity trends. Air transport has become the standard operational choice for key industries, rather than merely a discretionary upgrade. Developments across South Asia provide insight into why certain regions maintain persistently tight capacity conditions, even as overall global demand declines.

Electronics and pharmaceuticals are rewriting South Asia’s baseline

India’s export mix remains anchored in sectors where air freight is essential: electronics, pharmaceuticals, high-value components, and time-sensitive goods. Growth across major hubs—including Delhi, Bengaluru, and Chennai—reflects a manufacturing environment where speed, compliance, and reliability are integral to product requirements.

These factors help explain why freighter space remains under pressure across South Asia, even as passenger belly capacity continues returning across key international corridors. High-value industries are relying on air as the default mode, not an emergency alternative, creating a structural floor for utilization that does not fluctuate significantly with seasonal cycles.

India’s exports to China reportedly grew 33% between April and November 2025, primarily driven by increased shipments of electronics and pharmaceuticals. This rise underscores how tightly linked the region’s manufacturing ecosystem has become to air-first logistics strategies.

A recently announced U.S.-India trade agreement could add further momentum to these flows. Under terms reported by the U.S. administration but not yet formalized, U.S. tariffs on Indian imports would decrease from 25% to 18%, while India would eliminate tariffs on U.S. products entirely.

Two distinct demand profiles are now developing

India’s trajectory highlights a bifurcation that appears to be becoming more pronounced across the global air market:

Identifying the specific “air economy” that governs a given route is crucial for effective planning. Routes designated for essential cargo tend to exhibit consistent patterns and typically remain constrained. In contrast, optional routes fluctuate based on factors such as cost, urgency, and the presence of alternative options.

Two types of air freight demand

Planning ahead

India’s example provides a useful lens into the potential behavior of structurally high-value markets over time. In these corridors, capacity constraints are influenced less by seasonal fluctuations and more by the characteristics of the cargo. For shippers, this necessitates segmenting shipping lanes by cargo criticality rather than just origin-destination pairs.

As February progresses, lanes tied to essential industries are likely to maintain stable volume and sustained utilization, while cost-driven and discretionary lanes may continue to see wider swings in rates and available space.

Notable updates this month

Asia’s tech-weighted demand mix is creating a sharper pre-holiday split than usual

This month, Asia’s outbound exports are mainly focused on technology-related goods like electronics, semiconductor parts, artificial intelligence hardware, crypto-mining equipment, and solar products. This concentration appears to be supporting firm demand even as general cargo volumes ease.

Combined with the compressed pre-Lunar New Year window, this mix suggests short term tightness may be more influenced by sector composition than by volume alone. Monitor how this tech-driven concentration affects early-March capacity normalization.

Europe’s air market continues to soften as belly capacity expands faster than demand

Long-haul passenger schedules continue to add significant lower-deck lift across Europe, but manufacturing output and U.S. import demand remain muted. This widening imbalance continues to reinforce structural oversupply rather than creating short-term volatility. Rates remain under pressure, and the environment may favor shippers that can leverage flexible timing or opportunistic routings. Conditions suggest that even small demand swings could produce more noticeable rate movement than in past seasons.

Asia–Europe flows remain stable despite seasonal front-loading

Even with modest front-loading ahead of Lunar New Year, Asia–Europe lanes continue to show adequate capacity at major origins. Demand remains soft but steady, supported by ecommerce and general cargo flows, with capacity management keeping conditions balanced.

Short-term rate increases may occur as shippers position cargo before factory closures, but historical patterns indicate these effects tend to unwind quickly once operations resume. This stability may offer a brief planning window for shippers with Q2 alignment needs.

South America’s northbound stability is being reinforced by perishables and expanding long-haul lift

The ongoing seasonal demand for flowers, fruits, and fish provides a steady flow of goods moving north from South America. What stands out this month is how this baseline interacts with additional long-haul freighter capacity into both Europe and Asia. Together, these factors may support more consistent two-way flow, even as regional operational challenges persist. This may provide shippers moving mixed cargo profiles with more stable uplift options through the late-Q1 period.

South Asia’s airport-handling pressures point to future capacity shifts

While February demand remains steady, longer-term infrastructure changes—such as extended freighter restrictions at major hubs like Mumbai—are expected to redirect cargo flows later in the year.

This shift could concentrate volumes through Delhi, Bengaluru, and Chennai, tightening freighter availability on certain corridors even as seasonal patterns stay relatively stable. Shippers with recurring South Asia uplift may benefit from diversifying routings or securing early capacity commitments ahead of anticipated handling shifts.

Key takeaways

Source: https://www.chrobinson.com/en-us/resources/insights-and-advisories/north-america-freight-insights/feb-2026-freight-market-update/air/

Global air cargo rates have continued to rise strongly as stakeholders adjust to the dynamic and highly challenging conditions following the military attacks on Iran by the...

Driven by the direct impact of Jet A-1 fuel prices hitting a record high of nearly $200/barrel (a sharp spike from $95 at the beginning of the year), over 60% of international...

Vietnamese airlines are reviewing flight operations and preparing fuel surcharge plans in response to soaring aviation fuel prices linked to supply disruptions in the Middle...

Air charter rates have surged to “Covid-era” levels as the Iran conflict triggers a sharp capacity squeeze and volatile fuel costs, with brokers warning the market is being...

Many US logistics firms have their hands full with traffic triggered by the AI boom, with repercussions going well beyond data centre construction and outfitting to the energy...

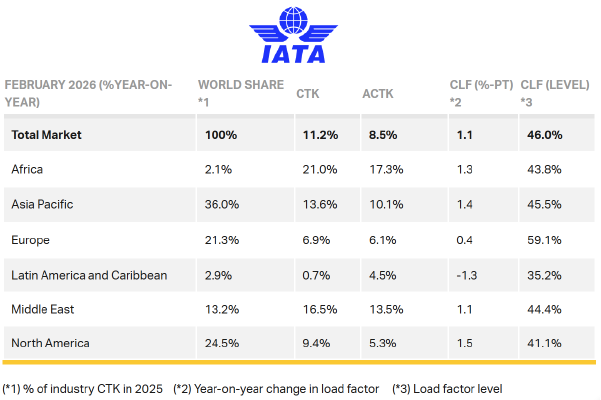

Total demand, measured in cargo tonne-kilometers (CTK), rose by 11.2% compared to February 2025 levels (+11.6% for international operations).

Beyond the immediate impact, the conflict in Iran highlights the need for resilient supply chains capable of quickly adapting to an increasingly uncertain global environment.

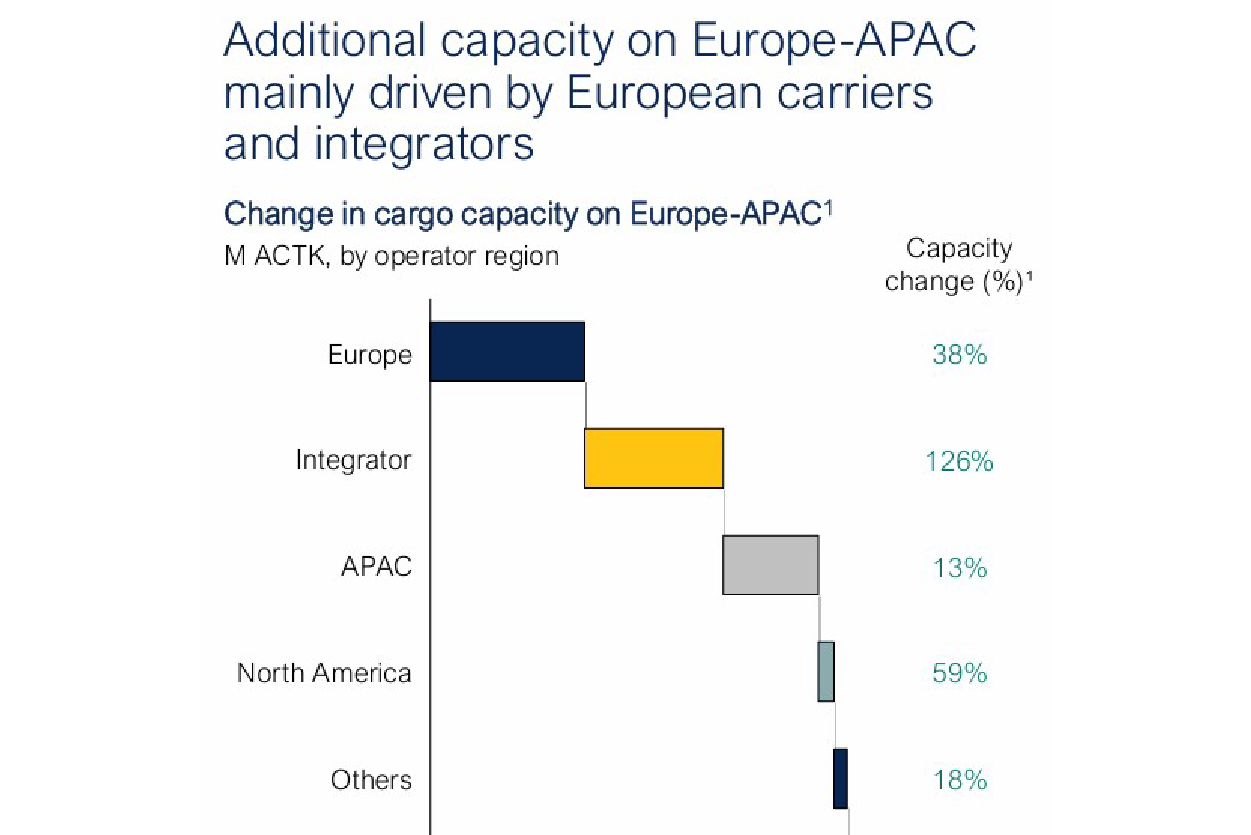

European Airlines and integrators have been the most active in adding capacity to the Asia-Europe trade lane to make up for the shortfall created by the loss of operations...

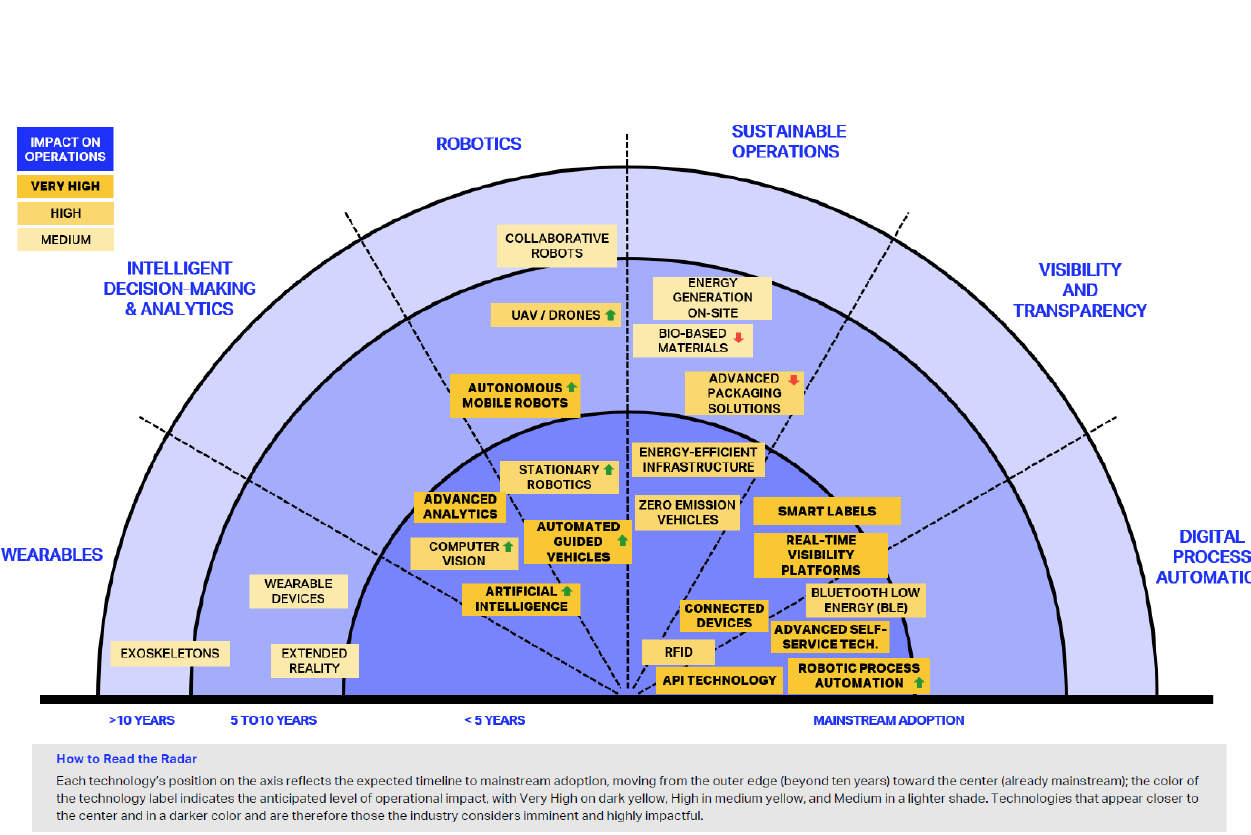

The global air cargo sector is undergoing a steady shift towards automation and data-driven operations, the International Air Transport Association (IATA) said in its 2026...

United Parcel Service Inc (UPS) opened a new US$100 million logistics center in Taiwan yesterday, its largest in the Asia Pacific, riding a wave of demand from tech companies.