Worldwide air cargo tonnages plummeted in mid-February, largely as expected, due to the Lunar New Year (LNY) holidays in China and large parts of east and southeast Asia, with chargeable weight falling by around -20% in the second and third weeks of February after rising for the previous six weeks.

According to the latest weekly figures from WorldACD Market Data, total worldwide tonnages dropped by -16% in week 8 (16 to 22 February) after falling by -5% the previous week, as public holidays and factory closures in key international manufacturing nations caused a sharp drop-off in cargo traffic, as they do every year around LNY.

This year’s LNY air cargo decline appears to be steeper than last year’s slowdown, when tonnages dropped by around -13% in the key two weeks around LNY 2025 – although last year was unusual in so many ways, and there was already some pre-loading taking place around this time last year ahead of anticipated changes to US tariff and de minimis rules. This year’s -20% decline is similar to that experienced around LNY in 2024, based on the more than 500,000 weekly transactions covered by WorldACD’s data.

Asia Pacific demand plummets

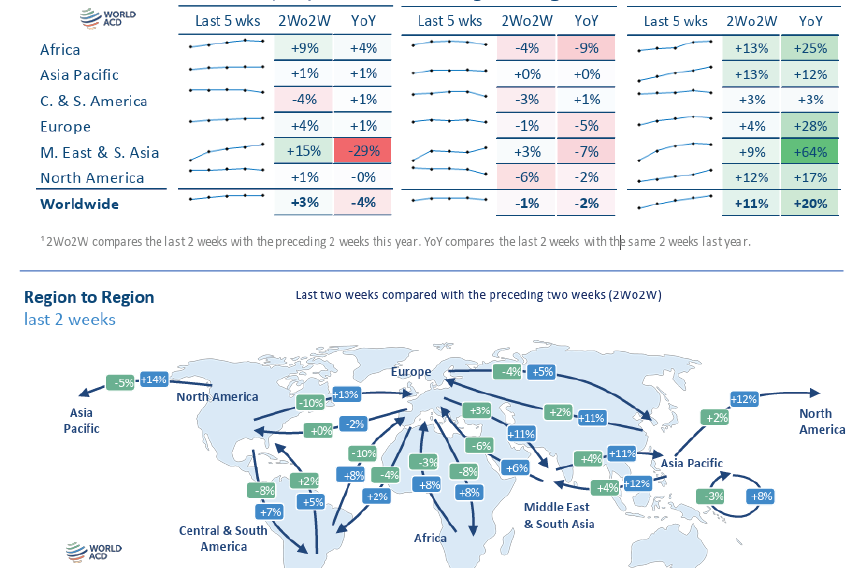

After only a -3% week-on-week (WoW) decline the previous week, in the lead up to LNY on 17 February this year, air cargo tonnages from Asia Pacific origins plummeted by -33% in week 8, taking them -20% below their level this time last year (when tonnages had already partially recovered after LNY, which took place two weeks earlier in 2025, on 29 January). Forwarders reported that there had not been a particularly strong pre-LNY build-up in demand this year, but capacity had remained relatively tight in week 8, for example from China, due to holiday-related capacity cancellations.

As a result, average rates from Asia Pacific origins remained more or less stable (-1%, WoW) in week 8 at US$3.05 per kilo, +6% higher than week 8 last year, based on a full-market mix of spot rates and contract rates. Worldwide average rates of $2.38 per kilo were down by -4%, WoW, but remain +2% higher, year on year (YoY).

The impact on rates of LNY was more visible when looking at spot prices from Asia Pacific origins, which dropped in week 8 by -5%, WoW, to $3.49 per kilo, although they were still slightly higher (+1%) than last year. Nevertheless, the WoW decline in spot rates from Asia Pacific was the main factor in a -4% WoW fall in global average spot rates in week 8, although they remained +2% higher compared with week 8 last year.

Ramadan effects

This year the Ramadan period started on the same day as LNY, on 17 February. Chargeable weight from Middle East & South Asia (MESA) also peaked in the first week of February, at +17%, YoY. Afterward volumes softened to still +10%, YoY, in week 8. From MESA to Europe and the US, there have been strong increases in traffic during the last three weeks from mainly Dubai, India and Bangladesh.

Spot rates from MESA origins had been relatively stable during this period, although in week 8 they rose by +4%, WoW, to an average of $2.55 a kilo – although they were -9% below their elevated levels of week 8 last year. From MESA origins to Europe, for example, average spot rates in week 8 rose by +6%, WoW, boosted by a +21% WoW spike in prices from Dubai to Europe.

Additional tariff uncertainty

Following a few months of relative stability, fresh changes to the US tariff landscape look set to bring further uncertainty and volatility to markets, particularly for US-bound air cargo. After the US Supreme Court this week ruled against the Trump administration’s International Emergency Economic Powers Act (IEEPA) tariffs, determining them to be unlawful, President Trump implemented a temporary new 10% global tariff (set to expire on 24 July), threatening to also raise it to 15%.

Trump also issued an executive order that maintains the suspension of ‘de minimis’ exemptions, although new rules will apply to postal entries, which become subject to the 10% global tariff until it expires, or until US Customs establishes a new entry process for postal shipments. It remains to be seen what the impact of these changes on air cargo flows will be.

Source: WorldACD

The jet fuel crisis is no longer a short-term disruption. Even if geopolitical conditions stabilise, the structural impacts on fuel supply chains, refining capacity and global...

Air cargo exports from APAC declined -3% WoW to Europe and -1% to USA.

China achieved a new milestone in making large-scale unmanned transport equipment as the domestically-developed HH-200 successfully completed its maiden flight on Wednesday.

Air freight rate levels from India to the Middle East have begun to moderate as airline schedules regain some normality, according to industry sources.

The US-Iran ceasefire offers near-term relief for air freight, but full recovery on Middle East routes remains one to two months away

The International Monetary Fund has released a sobering assessment of the global economic and financial stability outlook as conflict in the Middle East spikes energy prices...

European Union airports could start running out of jet fuel in the coming weeks unless the Strait of Hormuz opens soon.

Hong Kong International (HKG) has been named the busiest cargo airport in the world once again by Airports Council International (ACI).

For an industry historically optimised for speed and direct connectivity, the recalibration under way reflects a growing emphasis on resilience, redundancy and network flexibility.

The system will go live at 8 a.m. EDT to begin the electronic returns process for an estimated $127 billion in tariffs, the agency said Tuesday.