Widebody freighter conversions exceeded narrowbody conversions for the first time since 2009 last year as a result of narrowbody oversupply.

This pivotal change in the freighter conversion market was highlighted by aviation advisory firm IBA in its “The Freighter Outlook, Values & Conversion Trends” webinar yesterday.

“For the first time since 2009, we have seen widebody conversions exceeding narrowbody conversions,” said John Whaley, senior aviation analyst, IBA.

The reason for the switch was largely because of a slowdown in the number of narrowbody conversions, rather than an increase in widebody conversions.

IBA figures show that narrowbody conversions last year slipped to less than 20, compared with around 70 in 2024.

The slowdown in narrowbody conversions comes as a result of market oversupply, caused by a rush of orders in the immediate aftermath of Covid, when aircraft owners were looking for ways to utilise unused narrowbody passenger aircraft and the cargo market was in high demand.

While the widebody conversion market was larger than the narrowbody sector last year, this area of the market is not without its challenges.

In fact, the number of widebody conversions last year was actually down on 2024 levels, with 30 widebody conversions having taken place in 2025 compared with 40 in 2024 as the widebody sector battles with a lack of feedstock.

Whaley pointed out that widebody conversion stock had been retained in the passenger market in recent years as it was deemed too valuable.

“Widebody capacity is limited and it seems to be getting worse, not better,” said Whaley.

Whaley said the narrowbody oversupply is expected to eventually correct itself, but not until 2028 at least. This year, the company is expecting the number of narrowbody conversions to be just over 20.

Meanwhile, widebody conversions are expected to increase slightly this year, edging just above 30, with factors including more widebody programmes being available and improved feedstock as aircraft are retired from passenger operations.

“It’s well known that the narrowbody market has been dealing with the oversupply problem, so naturally you are going to see those conversion streams shrinking, so to speak,” Whaley added.

There were record passenger-to-freighter conversions in 2023. In comparison, 2025 was a quiet year, but the number of overall conversions in 2026 is expected to be slightly higher than in 2025, according to IBA.

Whaley said IBA does expect conversion activity to increase as this decade progresses.

“IBA’s opinion is that 28-30 (2028-2030) is when (the market will) see conversions across both (widebody and narrowbody) increasing.”

Programme activity increases

Meanwhile, there are plenty of new conversion programmes in the market, IBA has noted.

The 777P2F operator base is growing, said Whaley. “We are seeing the market expanding.”

In September last year, IAI’s first two 777-300ERSFs were delivered by AerCap to launch operator Kalitta Air, and in December, AerCap delivered the first of three 777-300ERSF to Fly Meta.

At the end of March, Challenge Group’s first 777-300ERSF (extended range special freighter), converted with IAI, became operational in its fleet.

Mammoth Freighters received Supplemental Type Certification (STC) from the Federal Aviation Administration (FAA) for its 777-200LRMF (Long Range Mammoth Freighter) freighter conversion in April.

Meanwhile, the company has continued to make progress on its 777-300ERMF programme and expects FAA certification of that variant later this year.

Kansas Modification Center (KMC) announced in January it had reached a cargo door milestone and expected to begin flight testing and the supplemental type certificate (STC) process for its 777-300ERCF freighter conversion programme in the third quarter of this year.

Jonathan McDonald, manager – classic and cargo aircraft and senior ISTAT certified appraiser, added there is “not enough” feedstock for 777-300ER conversions, but availability should improve in the 2030s.

Conversion diversity

Outside of 777 conversions, Whaley said the 767-300ER conversion market is “still going strong”, adding “Amazon and Cargojet have already taken some this year”.

He further stated: “Cargo Aircraft Management, part of ATSG are going to take some more before the year is done. That’s already confirmed.”

But he also warned: “Feedstock is becoming scarce for the type.”

The A330-200 and A330-300 are also playing a more prominent role in the market, said Whaley.

Israel Aerospace Industries (IAI) announced this month that it had completed primary structural work on its Airbus A330-300BDSF prototype and expected certification by the end of the year.

Whaley said: “The -200P2F is definitely gaining traction in China.” Customers include Air Cargo China, JD Air Cargo and ZTO.” Usage has been mainly domestic.

In 2025, there were 10 conversions of the -200. There has been more availability of the -200 feedstock as the -300 is more in demand in the passenger market.

However, said Whaley: “Overall, the -300 does remain a more popular type and we do expect that to show in the future.”

Additionally, 737 conversions remain active. In January, MRO company KF Aerospace gained certification for the world’s first Boeing 737-800 combi conversion.

Aeronautical Engineers Inc (AEI) is also developing a conversion programme for Boeing 737-900ER aircraft with a planned launch date of 2029.

Although Whaley pointed out: “There is no rush for that conversion as the narrowbody market is oversupplied. The timing is not crucial.”

Source: https://www.aircargonews.net/freighter-conversions-mro/2026/05/widebody-conversions-overtake-narrowbodies-for-first-time-in-over-15-years/

The biggest growth sector in air cargo could face significant challenges if the Strait of Hormuz remains closed.

The most valuable cargo in the world today is neither gold, diamonds, nor pharmaceuticals

IATA called for stronger implementation of global standards, a transition to modernised ground support equipment (GSE) and greater digitalisation in the ground handling sector.

Nearly 38,000 loading errors were recorded across global ground operations in 2025, alongside more than 29,000 aircraft damage events.

The recovery is uneven and increasingly shaped by changing tradelanes.

A group of US cargo carriers has called on the Trump administration to temporarily suspend taxes on jet fuel in response to rising prices caused by the Middle East conflict.

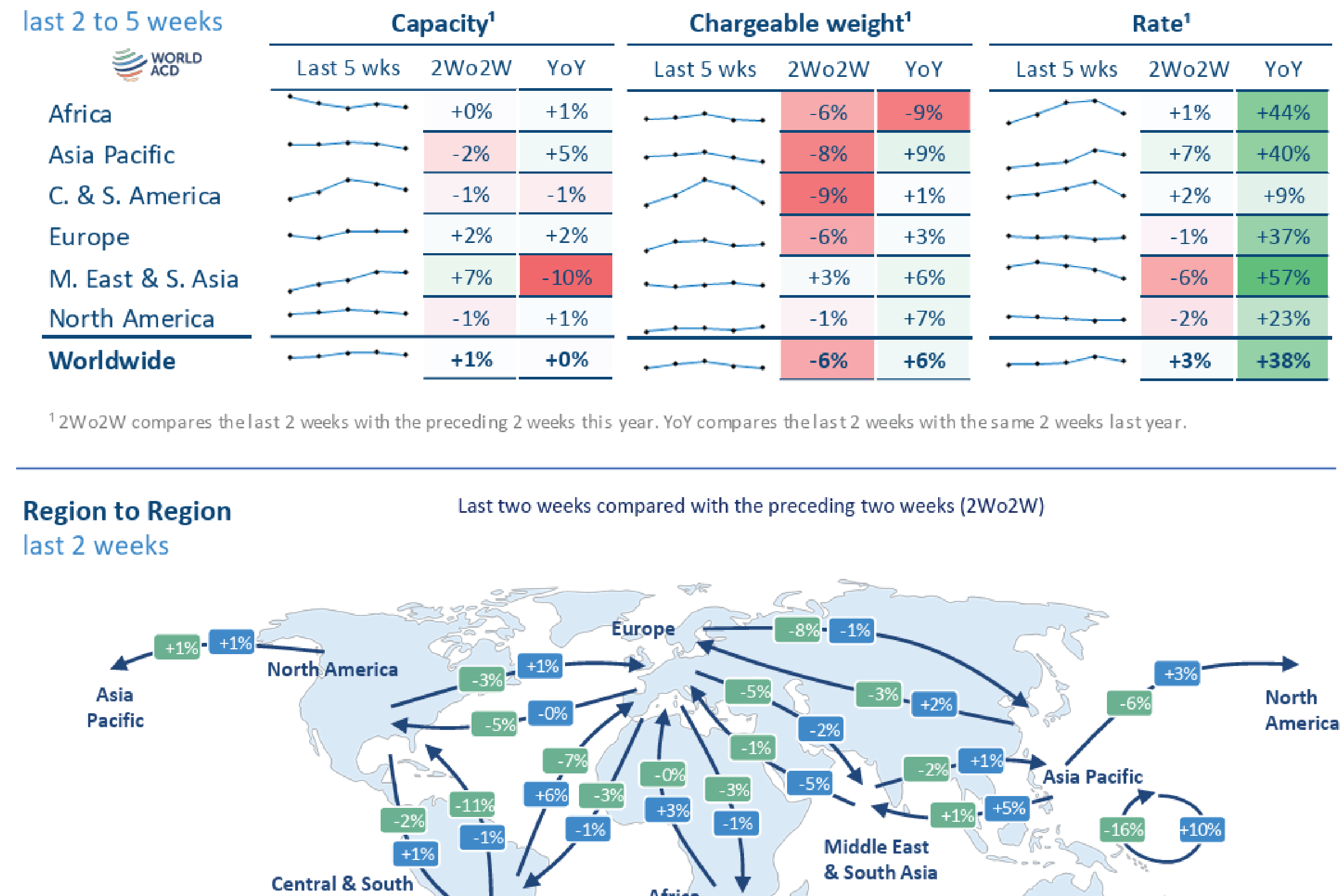

Volume from MESA dropped -5% WoW both to USA and Europe

India’s air cargo sector has achieved a major milestone, handling a record 3.72 million metric tonnes (MMT) in FY2024-25

The new Cargo Terminal 2, inaugurated on May 18, spans 16,864 square metres and will initially handle around 50,000 metric tonnes of cargo annually