The air freight market appears to be moving out of its acute crisis phase, with capacity recovering and fears of a near-term jet fuel shortage receding, although rates remain far above pre-conflict levels and tradelanes continue to shift.

After weeks of steep increases following the escalation of the Middle East conflict in late February, the latest TAC Index data suggests the market has started to cool.

The global Baltic Air Freight Index fell 4.9% in the week to 18 May, although it remained 30.4% higher year on year. TAC said the fall followed a short-term drop in jet fuel prices, by about 10% in early May, though prices remain roughly 80% higher than a year ago.

Freightos data points to the same trend: the panic phase has passed, but pricing has not normalised. Its global air index has continued to trend well above pre-crisis levels, while the Southern Asia-Europe lane, which was around $2.40/kg before the conflict, surged above $5/kg in April and has since eased only partially, settling around the low-to-mid $4/kg range by 20 May.

Public fuel surcharge data from Hong Kong also indicates the market is beginning to cool. Cathay Cargo’s long-haul fuel surcharge fell from HK$16.9/kg for the first half of May to HK$13.5/kg for the second half of the month, a reduction of about 20% in two weeks. DHL’s Hong Kong cargo fuel surcharge mechanism has shown a similar trend, with rates easing steadily from April peaks. However, both remain dramatically above pre-crisis levels seen earlier this year.

The result is a market that is no longer spiralling upward, but has clearly found a new, elevated pricing floor.

Capacity data from Rotate supports that picture. Freighter capacity grew 3% month on month in April versus March, reversing the previous month’s 2% decline. Week on week, however, growth slowed to 2%, down from 8% the previous week, suggesting airlines are restoring lift cautiously rather than flooding the market with capacity.

But the recovery is uneven and increasingly shaped by changing tradelanes.

Rotate’s data showed particularly strong month-on-month growth on Asia-Middle East, up 25%, and Europe-Middle East, up 16%, as the Gulf carriers get back to work.

Many other carriers are still avoiding the Middle East however. Cargolux CEO Richard Forson said the carrier had not changed its overall network strategy, but had removed most Middle East stops because of airspace and security concerns, retaining only Muscat.

But he also said global trade patterns were continuing to shift, with more production moving into South-east Asia and India.

“Tradelanes are shifting,” he said, adding that Asia-Europe, Asia-Middle East and Europe-North America remained among the strongest corridors.

The shift is being reinforced by the nature of cargo demand. Mr Forson said electronics, AI-related server infrastructure, pharmaceuticals, and ecommerce were all supporting the market.

“There’s a lot of electronics being flown… with the data centres being set up to facilitate AI development,” he said.

That demand has helped prevent a collapse in rates even as operational conditions improved. Seasonal Mother’s Day flower shipments from Latin America also helped absorb freighter capacity this month, particularly on Europe and North America lanes.

The latest TAC figures suggest some emergency pressure is now easing. Rates out of Hong Kong, India, and Korea all declined week on week, while Europe-US and Europe-Gulf markets also softened. However, pricing remains historically high, with Heathrow outbound rates, for example, still more than 40% above last year.

The market is, therefore, not returning to normal so much as adapting to a new environment.

Refineries in Europe, the US, and West Africa have shifted output towards aviation fuel, while airlines have rerouted networks, cut weaker services and concentrated capacity on higher-yield corridors. At the same time, carriers appear unusually disciplined on capacity deployment, helping prevent a rapid collapse in pricing.

While Mr Forson had warned that a prolonged closure of the Strait of Hormuz could still create fuel shortages and wider economic damage, he added that the immediate cargo market remained resilient, with “fairly healthy” demand and “fairly robust” yields.

In short, any feared further collapse in air freight availability has not materialised. But neither has the market returned to pre-crisis conditions. Instead, the industry appears to have repriced geopolitical risk permanently into the system.

Source: https://theloadstar.com/jet-fuel-fears-recede-but-air-cargo-settles-into-a-higher-cost-era/

The biggest growth sector in air cargo could face significant challenges if the Strait of Hormuz remains closed.

The most valuable cargo in the world today is neither gold, diamonds, nor pharmaceuticals

IATA called for stronger implementation of global standards, a transition to modernised ground support equipment (GSE) and greater digitalisation in the ground handling sector.

Nearly 38,000 loading errors were recorded across global ground operations in 2025, alongside more than 29,000 aircraft damage events.

Widebody freighter conversions exceeded narrowbody conversions for the first time since 2009 last year as a result of narrowbody oversupply.

A group of US cargo carriers has called on the Trump administration to temporarily suspend taxes on jet fuel in response to rising prices caused by the Middle East conflict.

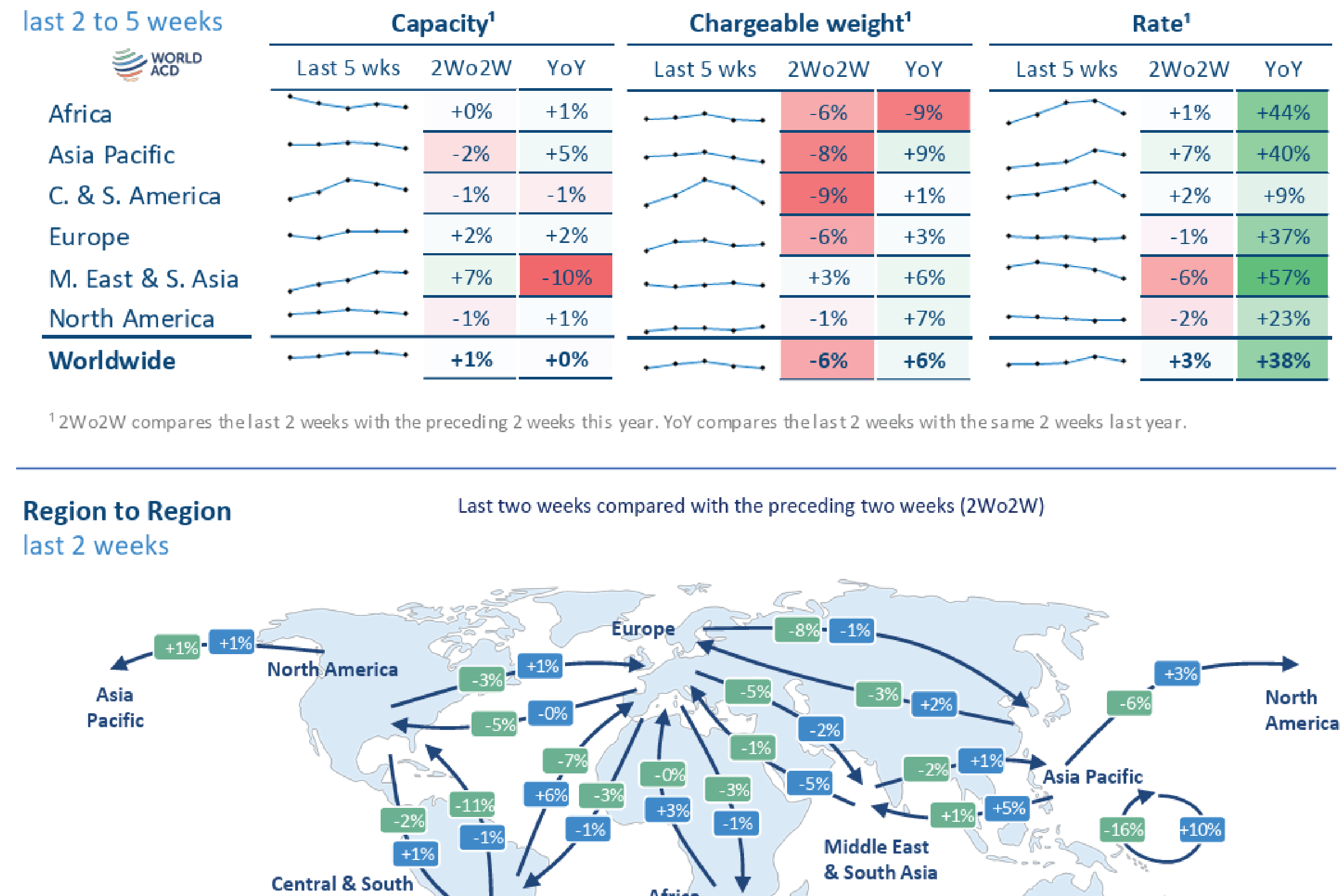

Volume from MESA dropped -5% WoW both to USA and Europe

India’s air cargo sector has achieved a major milestone, handling a record 3.72 million metric tonnes (MMT) in FY2024-25

The new Cargo Terminal 2, inaugurated on May 18, spans 16,864 square metres and will initially handle around 50,000 metric tonnes of cargo annually