Carriers are already tightening container shipping capacity ahead of the peak season, with blanked sailings increasing and reports emerging of rolled cargo at some Far East origins.

During a market update webinar, Freightos head of research Judah Levine said carriers were becoming more aggressive in capacity management, as they sought to defend freight rates against a backdrop of weak demand growth, elevated fuel costs, and continuing geopolitical disruption.

“We are already now seeing carriers increase blanked sailings,” he said. “And there have been reports even of rolled containers in some origins in the Far East.”

Destine Ozuygur, senior market analyst at Xeneta, told The Loadstar: “For blanked sailings, right now what we’re forecasting for June and July, is roughly on trend with what we’ve seen in previous years.

“Of course, that can change, because we see more and more coming in at the last minute every year.

“But April was crazy,” she added. “We saw, I think, a 37% increase year over year. So, in practical terms, they [carriers] are using blanks defensively and operationally.”

Mr Levine noted that lines were reducing capacity “to get rates to where they like them”.

Linerlytica reported that Maersk and Hapag-Lloyd had amended their Gemini Cooperation agreement “to modify the timing of discussions regarding potential seasonal blank sailings”.

While the carriers were authorised to blank sailings only during Chinese New Year or Golden Week holidays no later than 12 weeks prior to schedule, the revised agreement extends to cover Christmas, calendar new year “and/or other similar holiday periods”, and shortens the notice period to 6-8 weeks.

Currently the Gemini Alliance has the lowest sailing cancellation rate of the four main alliances, 2.8% compared with 15.9% for MSC, 17.1% for the Premier Alliance and 19.9% for the Ocean Alliance, according to Linerlytica.

It noted: “The move comes as Maersk’s ocean shipping earnings continue to deteriorate in the first quarter of 2026 and the Gemini partners continue to underperform its peers in terms of EBIT earning margins.”

Mr Levine said carriers appeared to be seeing varying degrees of success in managing rates on different trades. The transpacific had seen meaningful increases, while Asia-Europe carriers were primarily focused on preventing rates from slipping.

According to Freightos data cited by Mr Levine, transpacific spot rates have risen steadily since the start of the conflict. Asia-US west coast rates up around $1,000 per 40ft, to around $2,800, while east coast rates reached approximately $4,300 per 40ft.

Asia-Europe pricing has been more stable, with rates to North Europe around $2,800 per 40ft and to the Mediterranean near $3,500.

However, Mr Levine argued that even flat pricing represented a stronger market than would normally be expected during a low-demand period.

“We are seeing fuel costs being passed on,” he said.

Freightos data show that, during the previous low-demand period between peak season and Chinese New Year, Asia-Europe rates had fallen, to $1,700-$2,000 per 40ft. Current low-season levels remain significantly higher.

But despite tighter capacity management, Mr Levine warned that peak season demand could ultimately disappoint carriers if inflation and higher energy prices continue to weigh on consumer spending.

“There could be lower demand for freight,” he said, which would leave carriers “still facing those higher fuel surcharges”.

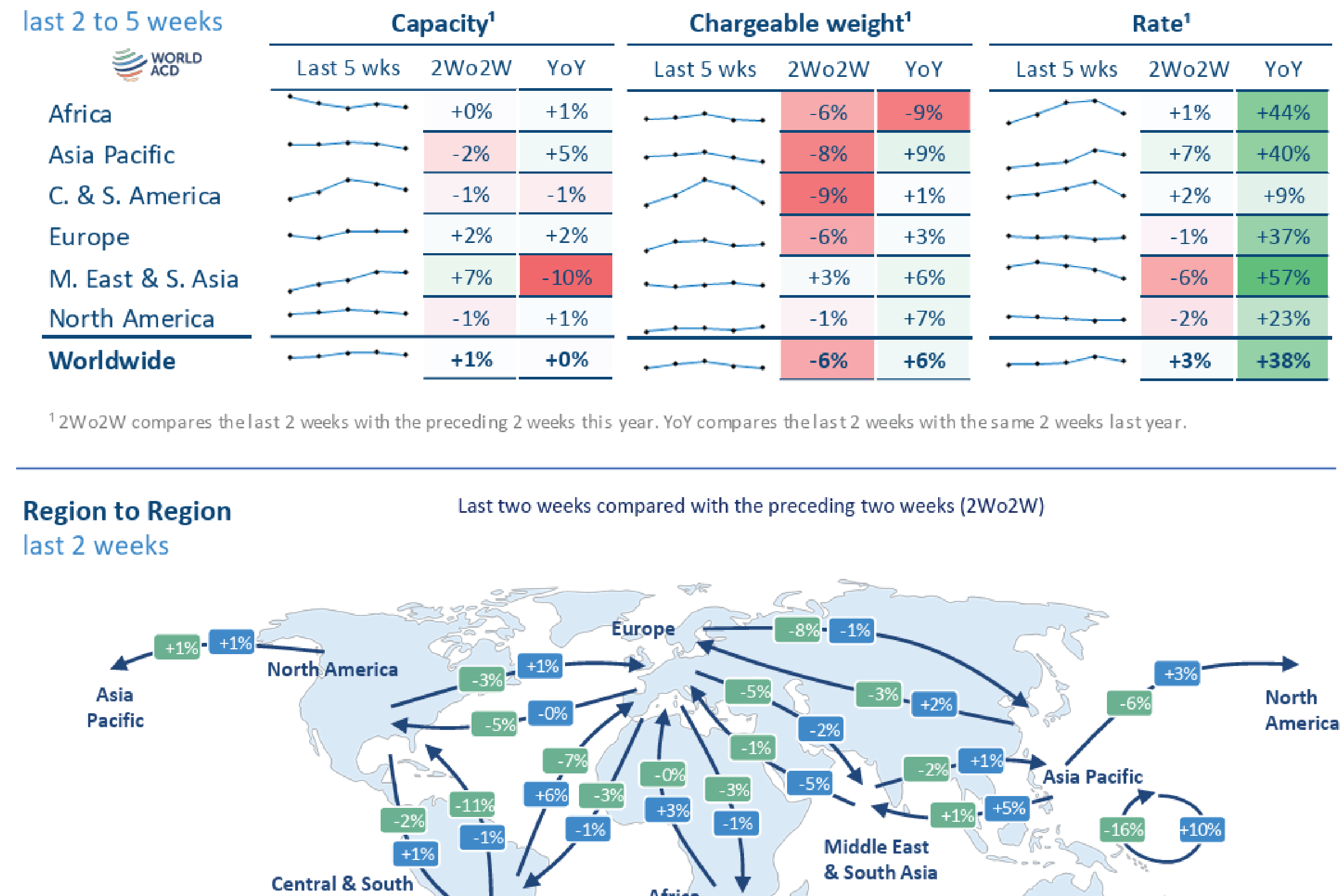

Volume from MESA dropped -5% WoW both to USA and Europe

India’s air cargo sector has achieved a major milestone, handling a record 3.72 million metric tonnes (MMT) in FY2024-25

The new Cargo Terminal 2, inaugurated on May 18, spans 16,864 square metres and will initially handle around 50,000 metric tonnes of cargo annually

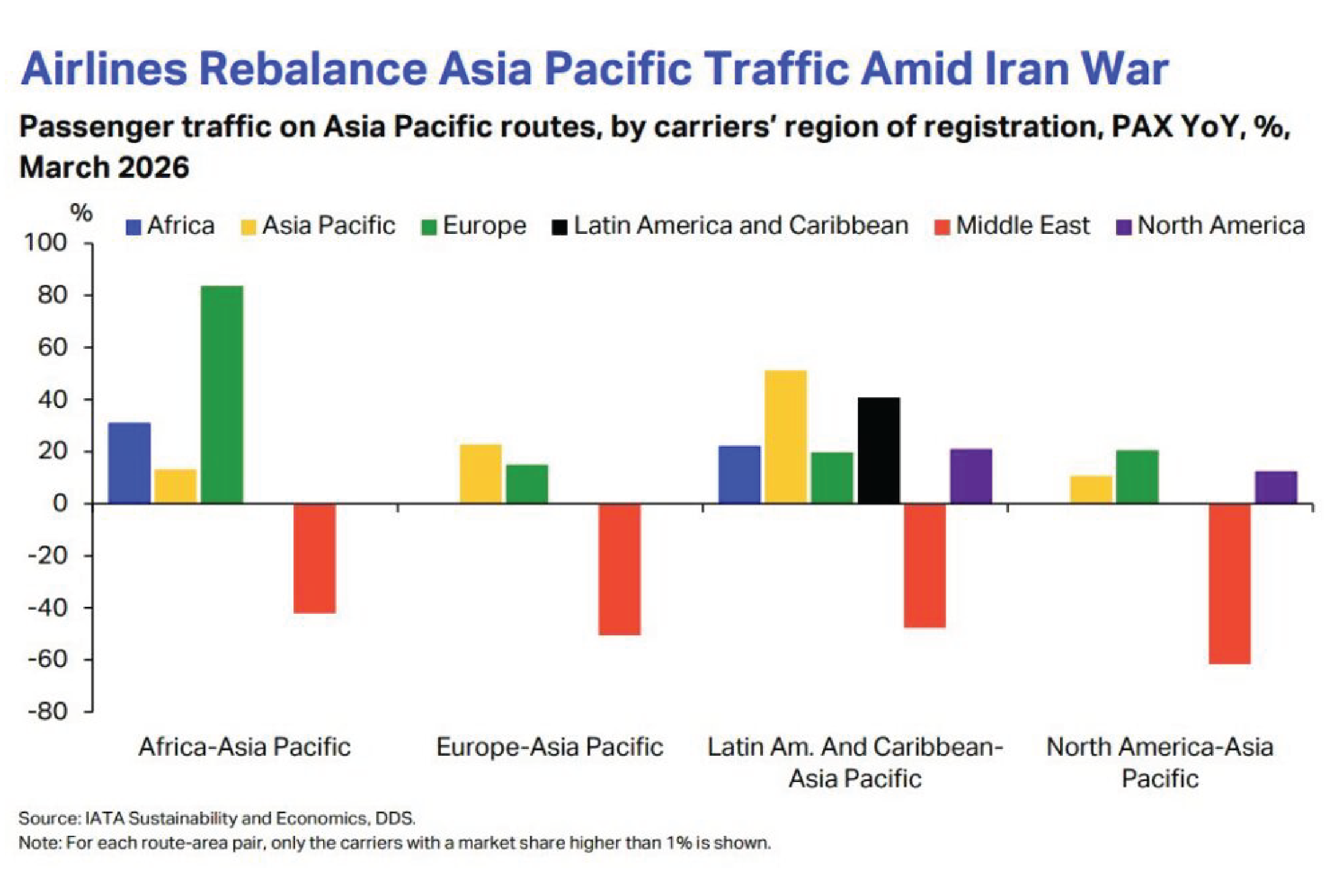

Asia Pacific carriers offset some of that with growth of nearly 23 percent, while European carriers grew by approximately 15 per cent.

Importantly, resilience does not necessarily mean sacrificing efficiency. The most advanced supply chains are learning how to balance both.

Semiconductor experience shaping supply chain thinking

Tight effective capacity, high operating costs, and ongoing geopolitical uncertainty are expected to keep air cargo markets unstable through the coming months

The two countries will use the board to manage bilateral trade for certain goods, and they also aim to resolve some non-tariff barriers in agriculture.

CMA CGM Air Cargo is looking to capitalise on ongoing air cargo demand growth out of Vietnam with the launch of a new freighter service between the Southeast Asian country...