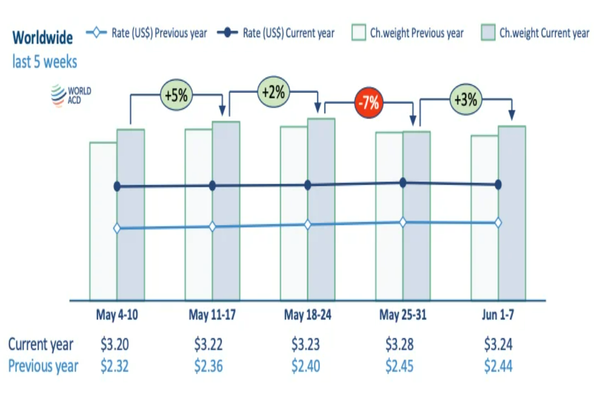

After several weeks of growth global airfreight volume dropped -7% in week 18 (April 27 – May 3) compared to the week before as the rush to move flowers in time for Mother’s Day ended and business activity slowed in several countries due to Labor Day. Despite the slowdown in volume and a rise in bellyhold capacity, pricing continued to climb.

Looking at the preliminary results for the full month of April, tonnage jumped +5% year on year (YoY), after dropping -4% in March, while global average rates increased from +12% YoY in March to +28% last month, arriving at its highest level this year at US$3.17 per kg.

With the exception of the Middle East & South Asia (MESA), air cargo tonnage declined week on week (WoW) from all origin regions during week 18. Chargeable weight dropped -9% from Central and South America (CSA) as well as Asia Pacific and Europe, the latest weekly figures from WorldACD Market Data show. The Asia Pacific region saw a convergence of Labor Day breaks with the national holiday in Japan (Golden Week) that weighed on demand.

Tonnage from Asia Pacific to Europe slipped -1% WoW, driven by double-digit declines from Vietnam (-17%) and Japan (-12%), while there was limited growth (+1%) outbound China, Hong Kong and Malaysia. Year on year tonnage on the Asia to Europe trade lane was up +7%, at the same level as the previous week. After three weeks of expansion chargeable weight from Asia Pacific to the US contracted -4% WoW, owing to double-digit drops from Japan, Indonesia and Vietnam, while tonnage from South Korea jumped +10%.

Chargeable weight from MESA to Europe slipped -3% WoW, owing to declines from Dubai (-13%), Bangladesh (-12%) and India (-5%). MESA exports to the US declined -2% WoW, as traffic from Dubai fell -20%, while volumes outbound India slightly increased (+1%) and outbound Sri Lanka jumped by +25%, WoW. Overall MESA origin traffic continued its recovery with a +2% WoW increase in chargeable weight, which was +4% higher YoY.

Airlines responded to the slowdown in demand by reining in freighter capacity, which shrank -2.7% WoW, a reflection of market conditions and the high cost of aviation fuel, which has nearly doubled since the end of February and caused carriers around the planet to cancel unprofitable routes. Despite increases of +2% from Africa and +6% from MESA (where Qatar Airways added about 4,000 tonnes of lift and bellyhold capacity out of Dubai rose nearly +10%), overall capacity was unchanged from Week 17, owing to cuts in CSA, North America and Asia Pacific. Year on year capacity was up +2% for the month of April, despite a -19% shortfall in MESA and flat growth in North America.

Slowing traffic does not stop pricing rise

Notwithstanding weakening demand and stagnating capacity, global pricing continued its ascent of recent weeks to US$3.29. It accelerated from +1% WoW growth in week 17 to rising another +3% WoW last week. Rates climbed +6% from Asia Pacific and +4% from CSA but retreated at low single-digit percentages in all other regions. This resulted in a +37% rise YoY overall, with increases across all origins ranging from +12% (CSA) to +59% (MESA).

Rates from MESA fell -4% WoW both to Europe and USA, retreating in most sectors, but remained elevated YoY, up +61% to USA and +63% to Europe. Out of Asia Pacific pricing to Europe was flat overall WoW. It rose in single digits from Thailand, South Korea and China but slipped in mid-single digits from Japan, Vietnam and Taiwan. To the US pricing from the region inched up +1% WoW, with single-digit drops out of Indonesia, Vietnam and Korea compensated for by single-digit increases from most other origins. According to forwarders, because of the high airfreight rates, some Asian shippers have resorted to sea-air transport to Europe via US West Coast gateways.

Middle East rebuild drives volume growth in April

After a -4% slump in March, global airfreight tonnage returned to growth in April, rising +5% YoY, close to the +8% YoY observed in the first two months of 2026, as Gulf-based airlines continued to rebuild their operations. Chargeable weight from the MESA region as well as from Asia Pacific are up +7% year on year. Inbound Gulf Area volumes recovered from -40% in March to -7% in April, YoY, which is similar to its outbound development. With the exception of origin Africa (down -5%), the other regions registered low single-digit growth over April 2025 volumes. Year to date tonnage was up +4%, led by Asia Pacific (+7%) and CSA (+5%).

Pricing in April was up +28% YoY across all regions, led by a +63% increase for origin MESA, followed by Africa (+37%) and Europe (+31%). For the first four months of the year pricing was +11% higher YoY, as rates increased in all regions, led by MESA (+20%).

Uncertainty over Middle East after renewed hostilities

The positive momentum seen in April was disturbed by a new outbreak of hostilities in the Gulf region on May 4, which caused short-notice airspace closures resulting in flight cancellations and re-routings. Forwarders warned clients of extended delays or space denials for general cargo. Subsequently the US administration reported signals of a possible agreement to end the conflict, but for now the situation remains in flux. One prospect that is certain is a continuing high level of airfreight pricing due to lasting high oil prices, as it will take months for oil production to regain pre-war levels.

Source: WorldACD Weekly Report

The launch of a dedicated air cargo route between Ezhou Huahu Airport in China’s Hubei province and Lahore marks the first time a direct freight air link has been established...

Although global sustainable aviation fuel (SAF) production is expected to increase by more than 26% in 2026 compared to the previous year, it will comprise just 0.8% of jet...

Freight forwarders are expected to see profitability remain under pressure despite a peace deal being reached by the US and Iran.

Promotions began in mid-May and run through June 20 to June 21. May retail sales fell 0.6% year-on-year. This year's event may provide clues on popularity of AI shopping tools

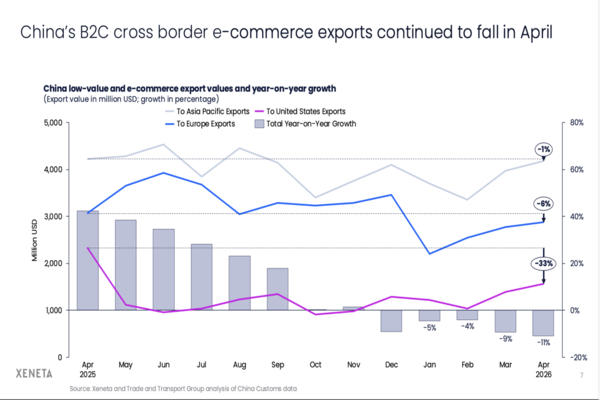

Chinese cross-border e-commerce exports continue to decline following regulatory changes in the US and increased scrutiny in Europe

Air cargo activity stepped up a gear and airlines redeployed capacity after a slowdown in the previous week caused by a convergence of public holidays in Europe (Pentecost),...

TIGHTENING capacity, earlier peak season demand and rising rates are putting increasing pressure on air and ocean supply chains in the strong Asia Pacific region, according...

The airline association said that this year SAF production is expected to reach around 2.4m tonnes, up 25% from 2025 levels. However, the growth rate is down from the 90%...

Transport logistic Southeast Asia and air cargo Southeast Asia 2027 will focus on supply chain resilience as global trade faces growing disruption from geopolitical tensions,...

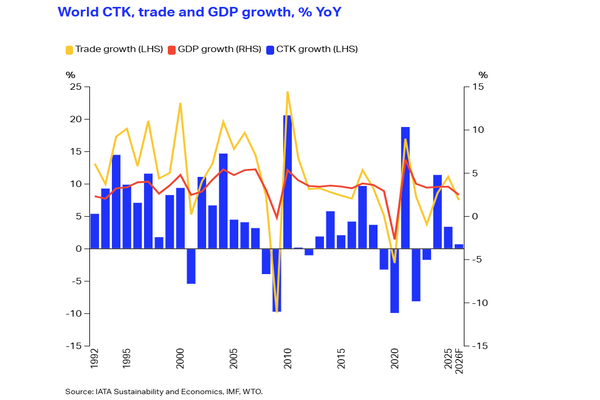

After a strong start to the year, cargo demand is now expected to grow by just 0.7% in 2026. Capacity shortages, especially in passenger bellyhold, are tightening the market...